Dear Friends,

Due to the Federal Reserve raising interest rates, the US Treasury yield curve has made headlines recently by inverting. An inverted yield curve is an unusual state in which longer-term bonds have a lower yield than shorter-term debt instruments. It is unusual as bonds with shorter maturities are supposed to yield less than bonds with longer maturities (as there is less risk involved with shorter maturities). According to LPL, yield curve inversion is likely going to be the phrase of the year in 2022.

Investors, strategists, and economists watch several different yield curves, but the 10-and-2 yield curve – or spread between the yield on the two-year Treasury note and the yield on the 10-year Treasury note – has been a strong predictor of past recessions. Anu Gaggar, Global Investment Strategist for Commonwealth Financial Network, says that the 10-and-2 yield curve has inverted 28 times since 1900, and in 22 of those instances, a recession has followed. If the Fed follows through with expected rate hikes, we will likely also see the 3-month/10-year close to inversion by the end of the year, which is even stronger evidence we could be in a recession in 2023/2024.

As you can see in the chart below, the yield curve is pretty steep until it hits the two-year maturity mark, but then it flattens out. This is an indicator of a potential recession.

Treasury.gov, Kiplinger

Treasury.gov, Kiplinger

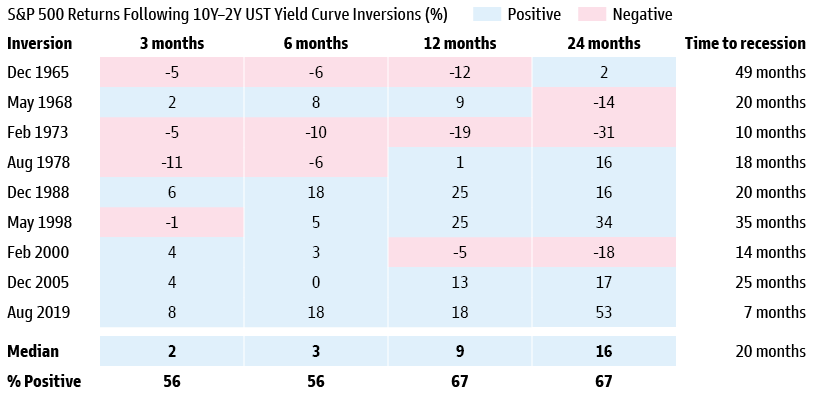

While an inverted yield curve has historically been a signal for recession, Goldman Sachs believes the curve may be more prone to inversions today, given low absolute yields, quantitative easing, low bond yields overseas, and elevated inflation. The historical time lag between an inverted curve and a recession has ranged from 7-35 months. In that time, the S&P 500 has continued to deliver positive returns on the median. Indeed, the S&P 500 Index was positive 67% of the time twelve months after a yield curve inversion, with a median return of 9%.

Goldman Sachs Global Investment Research

“The last four times the 2-and-10 yield curve inverted, the S&P 500 was up an average of 28.8% before it peaked,” writes Ryan Detrick, Chief Market Strategist at LPL Financial. The S&P 500 hit its ultimate peak an average of 17.1 months after the inversion, Detrick adds, while a recession started, on average, 21 months later.

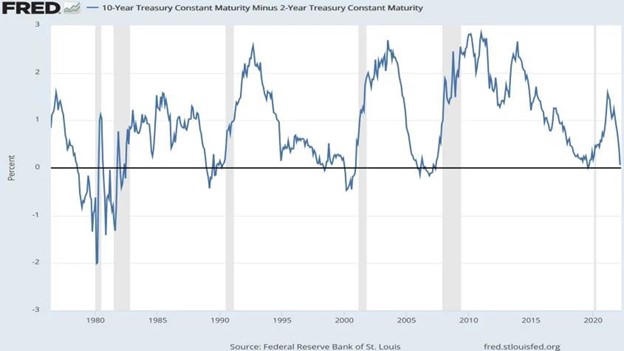

Have a look at the chart below, which shows the ten-year Treasury yield minus the two-year Treasury yield going back 50 years. Whenever the sum has gone negative, a recession (the shaded gray areas) has ensued.01335086

However, according to Dr. Ed Yardeni, President of Yardeni Research, he sees the Fed’s multiyear bond-buying spree as skewing the inversion data. “Our models show the flatness of the curve could be more a consequence of the Fed’s relentless buying of bonds, and the consequent growth of their balance sheet, rather than because of a looming growth shock,” Yardeni writes.

Equity investors should be mindful to not overreact when the yield curve first inverts as equity returns often follow. But, we still need to watch closely as it is a strong indicator of a recession later.

Please reach out with any questions.

Debbie